Blog

In-Space Manufacturing report from Traxcn

It finds there are around 15 main startups involved with orbital manufacturing technologies. And it is a market, it notes, shaped by long development cycles, infrastructure dependency, and high capital intensity.

Also, high-value microgravity manufacturing is identified as the “nearest-term commercialisation pathway”, while in-orbit assembly and infrastructure platforms represent longer-horizon industrial possibilities.

Other main findings include that all-time equity funding has reached ~$397m. Capital deployment remains episodic, however, with Varda Space Industries’ $187 million Series C accounting for 82% of 2025 funding. Such funding, from a single round, signals selective investor conviction rather than broad-based sector expansion, Traxcn notes.

Also, just one acquisition has been recorded to date and no IPOs. This indicates that “liquidity remains driven by strategic consolidation rather than demand-validated commercial maturity” notes the report.

Funding

Total funding has grown from around $270,000, in 2016, to $227 million in 2025.

Tracxn writes:

“The global ISM ecosystem has attracted approximately $397M in all-time equity funding across 22 rounds, reflecting selective rather than broad investor participation. Capital deployment has been volatile and milestone-driven, with funding peaking at $227M in 2025, largely driven by a single mega round, Varda Space Industries’ $187M Series C. This concentration signals a structural shift in investor behavior, where funding is consolidating behind technically credible operators demonstrating progress toward scalable orbital production, even as early-stage players continue to compete for a relatively thin pool of exploratory capital.”

Geography

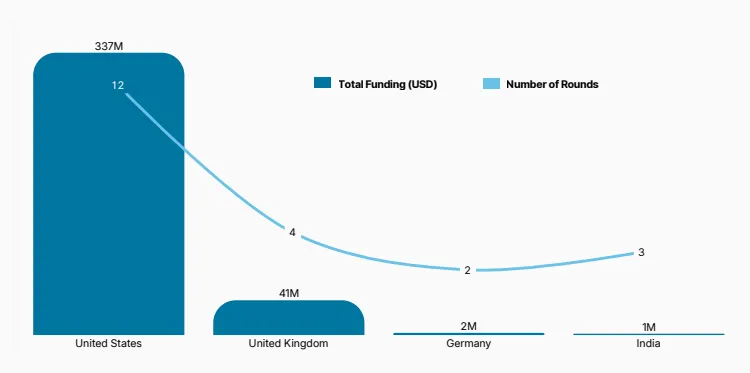

In terms of geographical spread, for the ISM ecosystem, the USA expectedly leads the way.

The States account for approximately 85% ($337m) of all-time funding. The United Kingdom emerges as a “credible secondary hub”, attracting roughly 10% of all funding, including through UK Space Agency initiatives (see UK companies to study manufacturing advanced materials in space and Regulatory clarity promised for space manufacturing of pharmaceuticals, for example).

Participation from Germany and India remains “nascent” say the report’s authors. But they note the potential for “gradual geographic broadening as domestic space capabilities mature”.

In-Space Manufacturing

You can download the report from the Traxcn website.

The full report covers company formation trends, investor participation, geographic concentration, commercialisation pathways and exit activity.

See all our Space content.