Blog

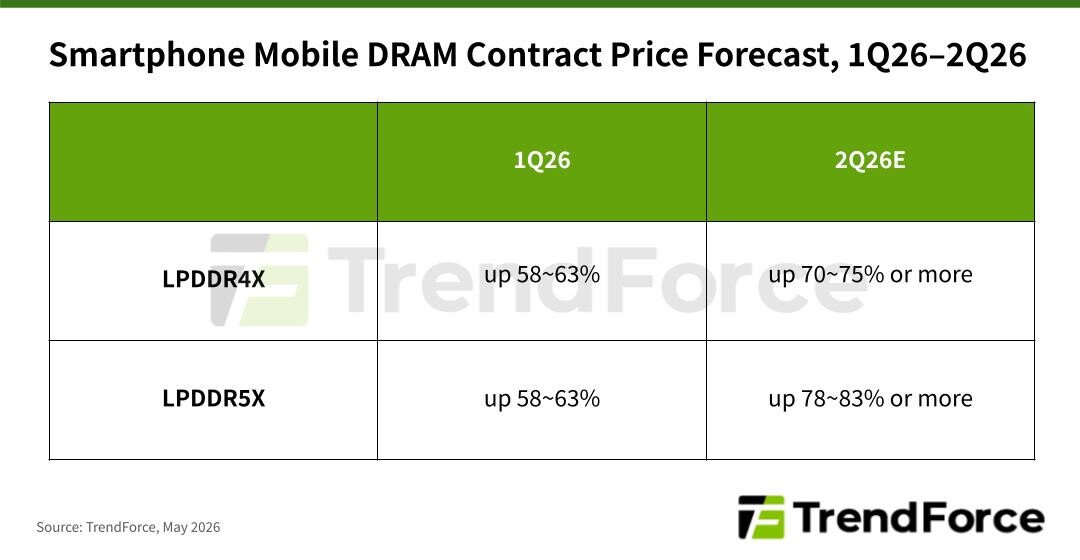

Mobile DRAM Contract Prices Continue Rising in 2Q26, Pressuring Smartphone Production

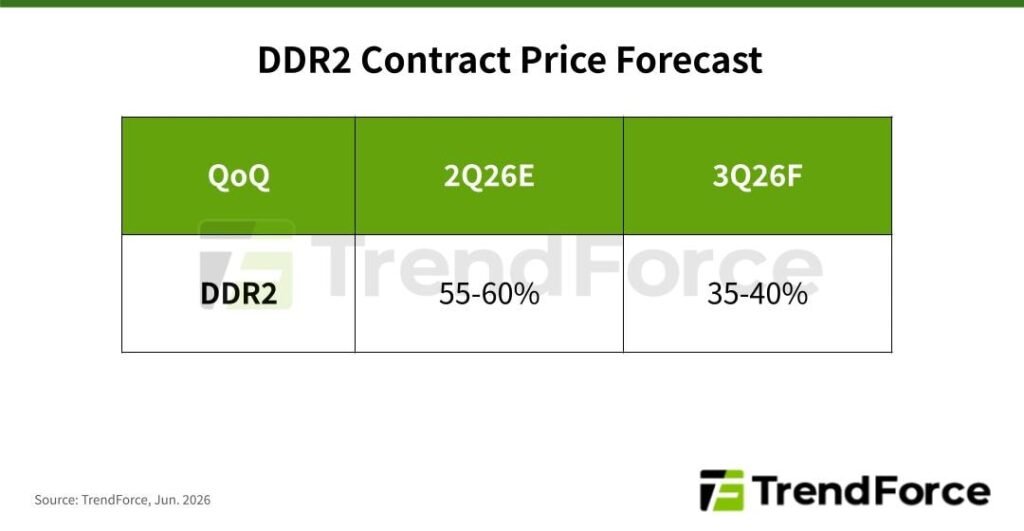

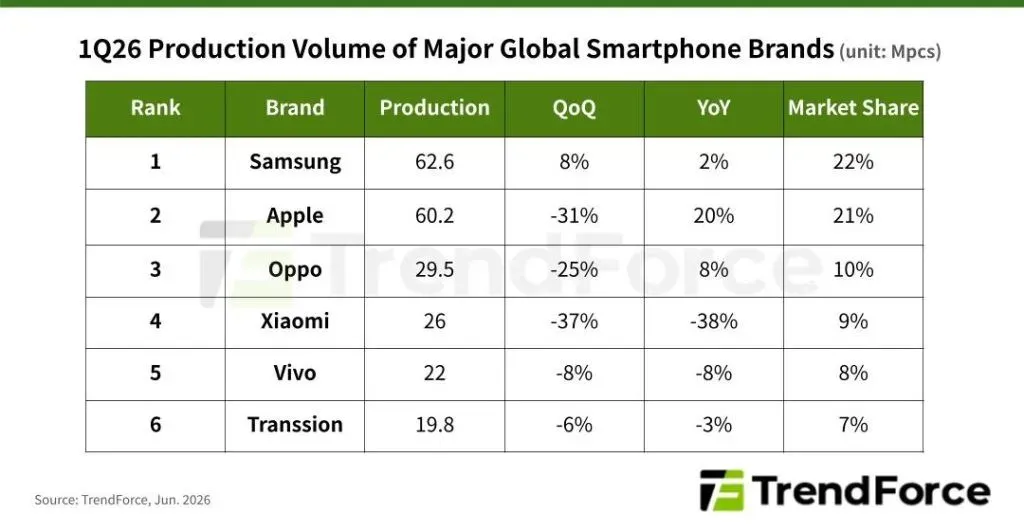

Notably, several consecutive quarters of steep price increases have significantly intensified cost burdens for smartphone vendors. Under such conditions, brands are expected not only to reduce total smartphone production in 2026, but may also struggle to fulfill the bit procurement volumes stipulated in the LTAs (or MoUs) arranged with suppliers at the end of last year.

High-price environment reshapes smartphone DRAM configurations, limiting high-capacity options

Persistently elevated DRAM prices are forcing smartphone makers to readjust memory configurations across product tiers. In the high-end segment, 12 GB is becoming the mainstream configuration while 16 GB adoption declines. Meanwhile, mid-range devices are reverting to 8 GB as the core specification, and entry-level models mostly settle around 4 GB.

Average smartphone DRAM capacity is still projected to increase to 8.5 GB in 2026—representing annual growth of 10%—despite the gradual phase-out of 2 GB and 3 GB models and reduced production of low-spec devices.

This supplier-driven memory price surge will continue exerting deep and sustained pressure on the global smartphone industry over the coming quarters.

TrendForce notes that smartphone brands are being forced to adopt more aggressive countermeasures, including working with app developers to reduce memory consumption and expanding service models that rely more heavily on cloud resources. Only by optimizing software and system architecture in parallel can vendors maintain operational resilience and competitiveness amid mounting cost pressures and slowing demand.