Blog

2025 Wafer Fab Equipment vendor revenue up 12%

The growth was propelled by the massive build-out of AI infrastructure, which surged demand for leading-edge logic, High-Bandwidth Memory (HBM), and advanced packaging tools.

The top five WFE manufacturers’ revenues grew 14% YoY in 2025 to $114 billion, driven by double-digit growth in both systems and service revenue according to Counterpoint Research’s Wafer Fab Equipment Tracker.

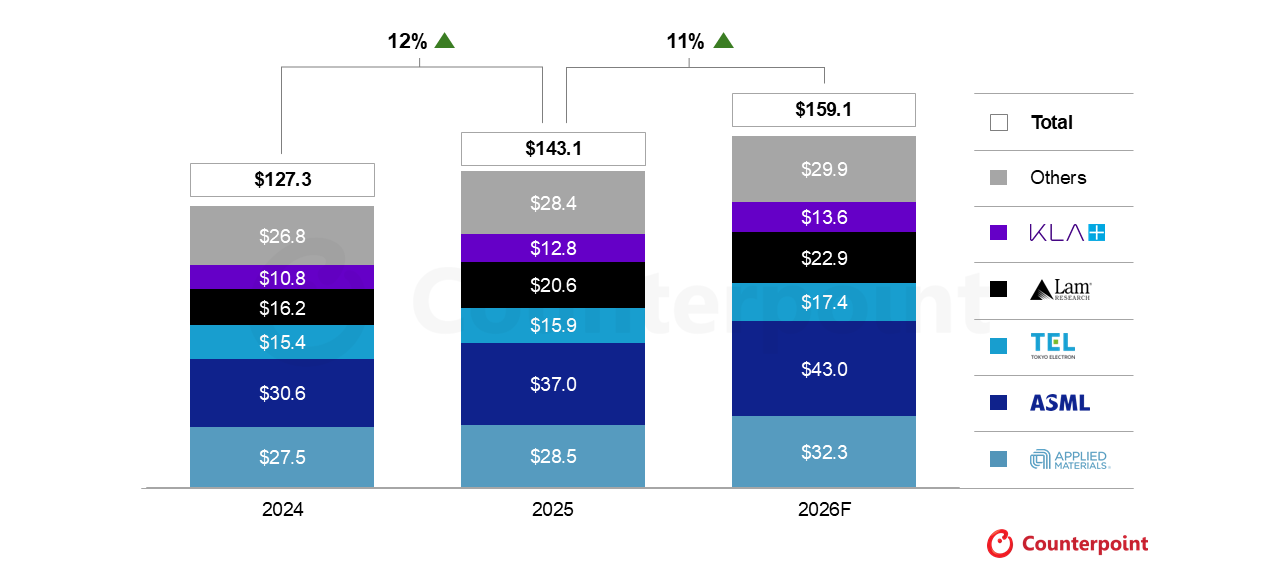

2026 Revenue Forecast by Equipment Maker (In $ Billion)

Source: Counterpoint Research Wafer Fab Equipment Tracker

WFE revenues are expected to grow 11% this year with growth weighted toward the second half of the year, driven by lithography, etch, deposition, process control and advanced packaging.

Segments like IoT, Auto, and Power sensors are expected to remain flat.

The main risks include physical infrastructure bottlenecks, geopolitical shifts, export controls and the timing of advanced technology ramps.

Foundry-Logic revenue grew 8% YoY and remained the industry’s primary engine, accounting for 65% of net system sales in 2025.

This dominant share was driven by foundry customers significantly increasing their tool investments to support the expansion of advanced chip production, especially for AI accelerators and high-performance computing.

Foundry 2.0 market’s revenue grew 16% YoY in 2025 to $320 billion. Unlike prior cycles, tied mainly to wafer starts, the next decade will see higher tool intensity per chip due to advanced nodes, chiplet architectures, and packaging complexity (CoWoS, 2.5D/3D).

Advanced nodes (5nm and below) shipment share exceeded 50% in 2025.

In the memory segment, revenue jumped 16% YoY for the full year. Although YoY growth in Q4 2025 remained flat, it saw a significant 15% sequential increase from Q3, signaling a robust expansion in NAND and DRAM capacity as suppliers race to meet demand for high-density, AI-optimized memory mainly driven by HBM demand for AI server compute ASIC and HBM base die transition to logic from DRAM process.

Further, HBM4 marks the first major architectural shift in high-bandwidth memory since inception/HBM2E, transitioning the base die from a traditional DRAM process to a logic process node. HBM4 is likely to hit the market in 2026, providing 2048-bit standard interface with data transfer rates of up to 12.8GT/s.

According to Counterpoint Research’s Memory Tracker, HBM4 and HBM4E is likely to constitute 79% of the total HBM shipments in CY 2027. Furthermore, revenue from memory is expected to be strong as customers transition to their next nodes to support latest-generation HBM and DDR5’s adoption across AI infrastructure will drive increased tool shipment.

This transition will increase lithography steps per wafer, EUV layers penetration increase, and litho demand per wafer grows faster, subsequently increasing deposition, etch and process control intensity.

China’s share of WFE revenue from the top five manufacturers fell to 32% of net system sales in 2025. This reflects a transition toward a more “normalized” market distribution, as geopolitical export controls and a shift in regional fab spending took effect. However, this decline was increasingly offset by aggressive leading-edge capacity additions in other global hubs.

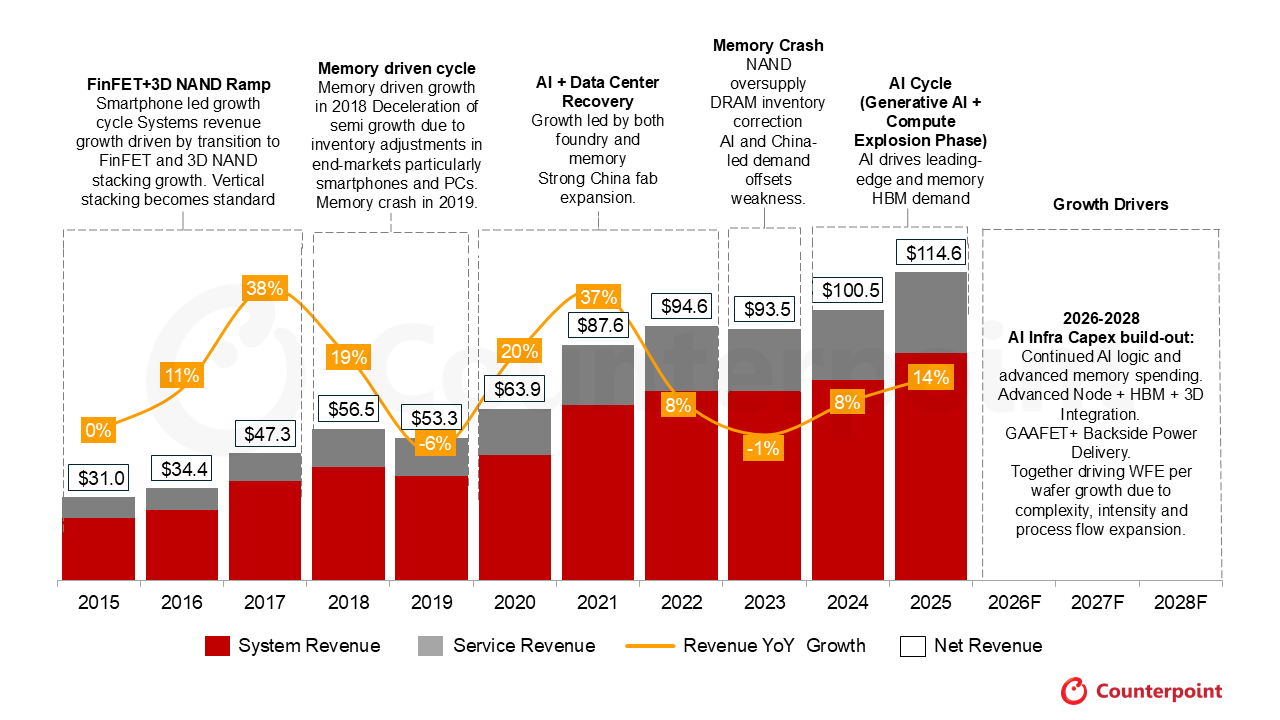

WFE spending has expanded dramatically over the last 10 years, with revenue from the top five vendors growing at 14% CAGR (2015-2025). This period marks the industry’s most capital-intensive era, characterized by a fundamental shift from capacity-driven capex to technology-driven capex. This growth reflects not only higher wafer capacity additions but also a structural increase in equipment intensity per wafer.

Between 2015 and 2025, WFE spending grew due to the combination of foundry-driven advanced node scaling, memory transitions such as 3D NAND and HBM and increasing equipment intensity across lithography, deposition, etch, and metrology to address the complexity of advanced node manufacturing.

This structural step-up in capital intensity across semiconductor manufacturing, has set the stage for continued growth through the second half of the decade as the industry moves toward 2nm logic, advanced packaging, and increased AI infrastructure capex.

Top 5 WFE System and services Revenue in $ Billion, YoY (%) Growth 2015 to 2025

Source: Counterpoint Research Wafer Fab Equipment Tracker